Humankind is well capable to feed itself – a statement that was doubtful a couple of decades ago but, thanks to the “green revolution” of the 1960s, is now a fact. Yet, we have been falling short of realizing this fact.

Sure, recent years’ disruptions of worldwide food-production systems – COVID19-pandemic; Russia’s attack-war on Ukraine (the world’s two largest producers of grain) – come to mind.

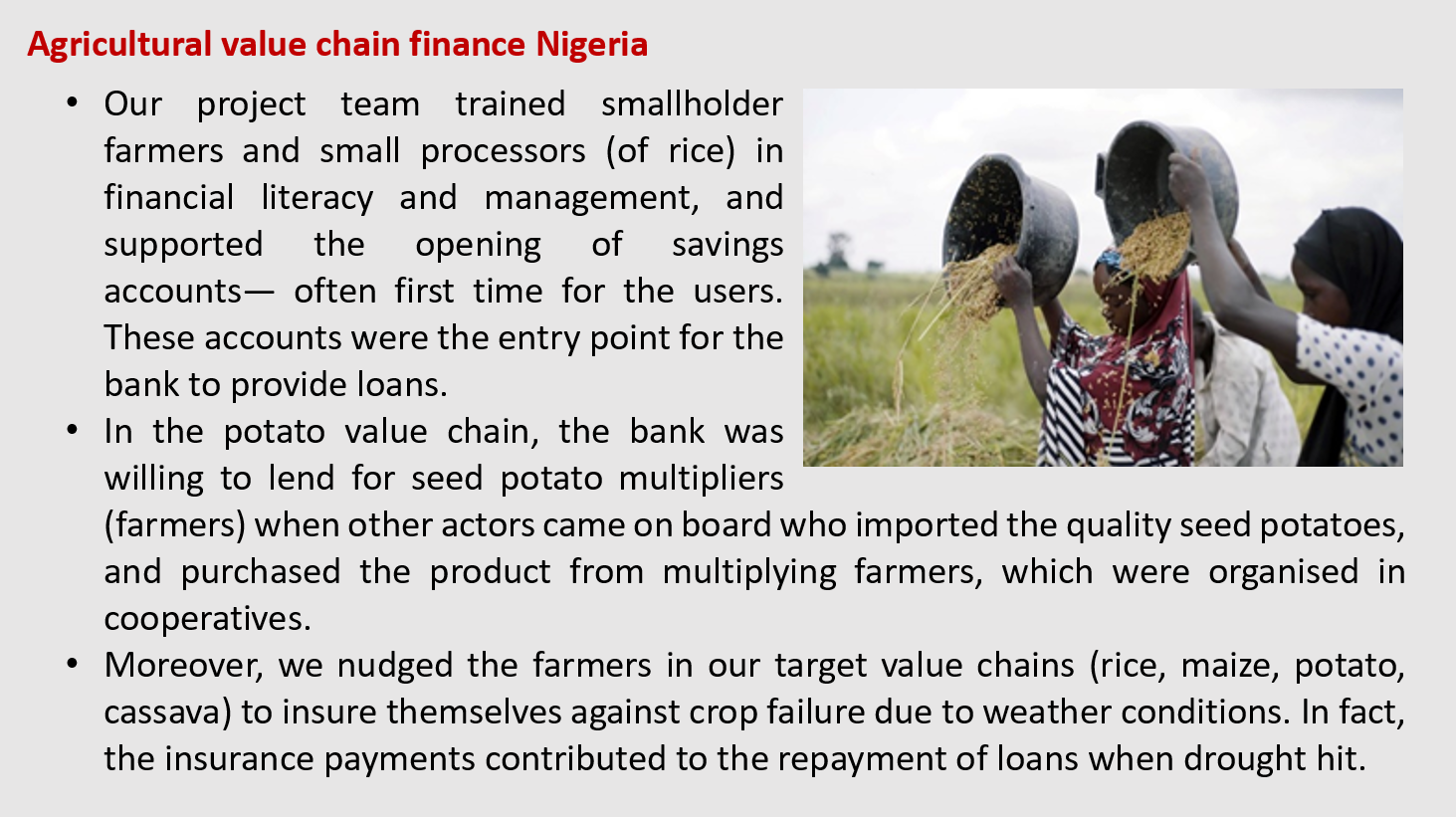

Here, we would like to discuss a more granular challenge – agricultural finance. Finance is a critical element of food production, because producing efficiently requires investment— investment in:

- Inputs, e. g. improved seeds;

- Storage and processing capacity;

- Agricultural management capacity;

- Climate-smart agricultural methods; these are usually subsumed among the above, but we suggest to consider them on their own.

GOPA AFC is one of the players who have worked on “both sides” of agricultural finance (AgFin) for over 30 years: On one hand, building capacity of financial institutions to understand how to finance agricultural activities and how to manage agricultural (credit) risks. On the other hand, supporting agricultural producers and processors to introduce improved methods and inputs, and to manage their agri-businesses to grow and to be bankable.

From our work, we find that the following are the three building blocks of successful AgFin operations:

Financial Institution (FI) strategy: A strategy may take the form of a paper or just a board minute, or it may be implied in a policy. Be that as it may, the important point is that the strategy is in the heads and behaviours of leadership. That means commitment and dedication from the top drive tracking of progress and allocation of resources. It also means there is resilience when things go less well than expected (they are bound to at one point or another).

A dedicated AgFin operation: Financing agricultural activities requires specific skills, specific tools and timing, and specific products. It cannot be a “by-the-way” or “also-do” activity of the microfinance or SME-lending staff and managers. Building such an operation requires resources over time. See a more concise discussion about the HR-Management implications, here.

MIS and IT to track it all: As the adage goes, what does not get measured, that does not get done. So FIs need to make changes to their MIS to track their agricultural lending activities and to analyse their performance adequately.

However, in the practice of African FIs, we find that recurring challenges of AgFin are:

Bringing the three together, i. e. having strategy, dedicated operation, and MIS/IT-support re-inforce each other. In our experience, a dedicated institutional change management process (ICMP), championed by senior manager(s) across departments, is usually required.

Agricultural Risk Management; bankers presume that agriculture is too risky. Some of them do not have the mindset, and many do not yet have the skills to assess agricultural risks systematically. When they acquired both, they may find they can take on more risks from agricultural customers than they expected, because there are ways of managing them (see e. g. climate smart agricultural methods discussed below).

It is noteworthy that in many markets, e. g. West-African Monetary Union (WAMU), the central banks and/or regulators do not make any allowances for capital (risk weighing) requirements for agricultural credit; so that any such lending is automatically expensive compared to other asset-classes. Unless the bank finds the right partner, for example an innovative player such as Aceli Africa who provides first-loss cover for the AgFin portfolio.[1]

Partnership Management; AgFin is successful where the bank can act in concert with other actors along the agricultural value chain. These actors provide a combination of enterprise management skill enhancement, financial literacy, market intelligence, and agronomy and livestock production technical assistance. They thus provide comfort for the lender. They also generate cross-selling opportunities of financial products.

Moving from input finance to asset finance: If the scale of agri-business operations is to go up, this requires assets such as machinery (e. g. combine-harvesters), cooling or drying facilities as well as management systems; e. g. for out grower schemes. Banks are often reluctant because capital cost rises (a larger loan amount, bound over a longer period). Yet, these loans are supported by tangible collateral.

Aligned cash-flows, particularly timely disbursement: Time and again, loans go bad because their repayment schedules are at odds with the cash flow cycles of the underlying economic activity. For agricultural production, meaningful grace periods are important. Even more important might be – and certainly more often missed in practice – that loan decision and disbursement processes are aligned reliably with the planting and weeding periods through the crop cycle. Whenever this fails, either the cost for the farmer goes up, as she uses some means of (usually expensive) intermediate finance, or the cultivated area is smaller than intended, or the applied fertiliser is less than required, because of cash-constraints. Moreover, the loan when received is used for something else than the agricultural activity, because its time had passed. Hence there is the risk of over-indebtedness of the farmer and excessive credit risk for the FI.

Climate-smart agricultural methods: Climate-risks make agricultural activities more difficult and affect cash flows, and thus credit repayments. Climate-smart agricultural methods mitigate these risks. In case of organic agriculture, they may also lead to higher sales margins of the farmer.

Moreover, FIs are increasingly called upon to have Environmental and Social Governance (ESG)[2] systems that track the FI contribution to reducing negative environmental and social footprints.

Climate smart agricultural methods are new to most farmers, as are ESG-systems to most banks. The demand for both has been going up among the international donor community. GOPA AFC has been implementing technical assistants for both in many countries in Africa and beyond, e.g the KfW financed biodiversity project in Uganda.

Outlook and Opportunities

Agricultural finance is one of the most important and exciting fields of financial sector development; as it sits at the intersection of food security, inclusive growth, and climate adaptation.

GOPA AFC supports financial institutions to improve and expand their AgFin products in many countries in Africa and Asia. Currently we are implementing for example projects on agriculture finance in Tanzania, Uganda and Tunisia, on horticulture finance in Uzbekistan, and on value chain agro finance in Kyrgyzstan and Tajikistan.

We have also distilled these experiences in an Agriculture Finance Brochure and in an e-learning course that covers, over 4 modules, the basic competencies that loan officers and middle managers require to run an FI’s AgFin operation.

We are looking forward continuing our work in the critical field of Agriculture Finance. We are committed to assisting financial institutions in tailoring their services to meet the unique needs of agribusinesses, and concurrently, guiding these businesses towards better bankability. Together, we can cultivate a more sustainable and prosperous agricultural landscape.

For more information, please contact: Oliver.Schmidt [at] gopa-afc.de or David.Odongo [at] gopa-afc.de.

[1] Also known as environmental and social management system (ESMS).

[2] Aceli's model is an adaptation of the Social Impact Incentives (SIINC) model co-created with Swiss Agency for Development & Cooperation (SDC) and Roots of Impact to SME finance in Africa. It is a donor-funded intermediary platform to provide smart support and incentives to commercial lenders and impact investors to lend more to agricultural value chains, particularly SMEs in Africa, than these lenders would otherwise be willing to fund given risk and profitability concerns. Among others, Aceli deposits a percentage of the value of each qualified agricultural loan in a reserve account available to cover the first losses in the lender's portfolio.